![[Case Study] GE FastWorks Transformation](/_next/image?url=%2Fblog%2Fposts%2Fge-fastWorks-transformation%2Fimages%2Fge-fastworks.png&w=3840&q=75)

Summary

Our team wrote a case and analysis of GE’s FastWorks initiative. At the time of its inception, GE was one of the most valuable and impressive companies of the past century. In many ways, GE was the poster-child of the multinational conglomerate business model. And yet, with FastWorks, the CEO was seeking change. Borrowing concepts from Silicon Valley titans like Eric Ries, FastWorks sought to redefine how GE identified, executed, and financed products. The result? Massive layoffs, GE’s stock lost half its value, and its CEO, Jeffrey Immelt, was forced to step down. What happened? Well, that's what we found out.

Section 1: Case Study

The Welch and post-Welch Eras at GE

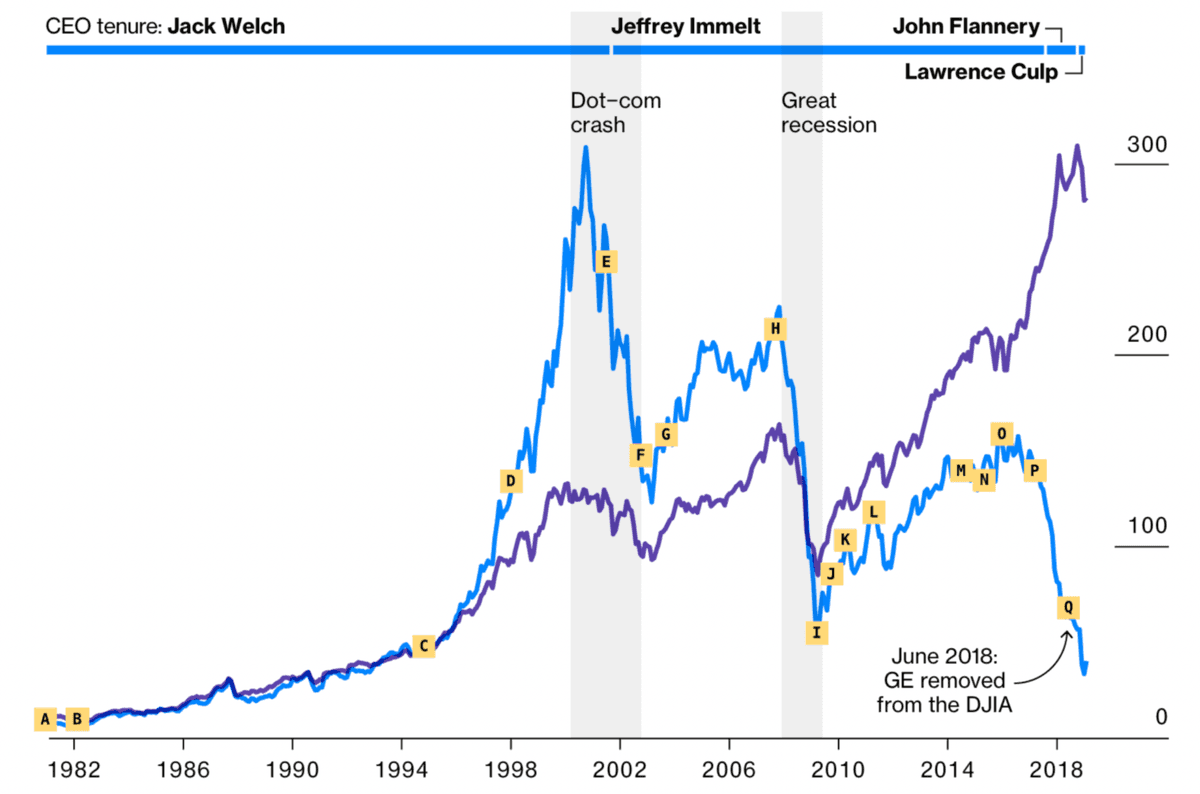

General Electric began its meteoric rise to the top of markets in 1981 with the placement of its youngest chairman and CEO, Jack Welch.[1]

Welch was an ambitious idealist whose early strategy focused on aggressive simplification, internal efficiency, and performance management. Shortly into his tenure, Welch disassembled GE’s leadership team and corporate structure as left by his predecessor, Reginald H. Jones.[2] Welch intended to dismantle bureaucracy and improve communication org-wide. He believed that involving employees in GE’s myriad business processes and manufacturing workflows would greatly benefit product quality and organizational productivity. As such, in 1995, Welch adopted the Six Sigma methodology that was developed at Motorola nearly ten years earlier.[3] A great deal of energy and investment was placed on increasing both quality and operating efficiency across GE’s various business units. Within three short years, GE’s revenues reached $100 billion for the first time in its history. However, this was primarily the result of GE transitioning away from its earlier business models—not a consequence of Six Sigma or increased manufacturing excellence. Welch transformed GE into a $100 billion conglomerate via a series of unjustified, continuous acquisitions. While this strategy delivered exceptional, short-term operating results, Welch's long-term vision and GE’s overall sustainability would soon be taken to task. By 1998, GE had holdings spread across all sectors and industries, including but not limited to aerospace, appliances, credit and mortgage services, insurance companies, media, plastics, power, information technology, and transportation.[4] GE’s once seemingly fail-proof strategy began to falter and decline in 2001 when the dot-com bubble finally burst. At the precipice of GE’s market capitalization, an unlucky Jeffrey Immelt would step in to take the reins from then-CEO Jack Welch just as the world’s developed markets were collapsing and the US began its war on terror.

Though Immelt recognized the challenges inherent in GE’s operating model, he was unwilling to altogether deviate from its extant growth strategy of mergers and acquisitions. He would spend over $175 billion across 300 M&As—though such behavior would yield diminishing returns in the post-Welch era.[5] GE was now competing with many firms that were emulating its myopic strategy—driving acquisition prices ever higher due to increased competition. Purchasing attractive companies for bargain prices would no longer serve as a viable business model for GE.

GE’s slight and subsequent recovery from 2003 to 2007 was short-lived. A global recession would once again cause its market capitalization and stock price to plummet. Amidst the worst financial crisis since the Great Depression, GE received $139 billion in government loan guarantees to shore up its failing and over-leveraged capital arm, alongside raising $15 billion via an emergency stock sale—a fifth of which was purchased by billionaire Warren Buffett.[6] It was unlikely that GE would survive the crisis without the intervention from Buffett and the US government.[7]

GE’s outstanding debt would peak at more than $500 billion in 2008.[8] Over the course of the great recession, GE’s stock price would fall from a high of $42 in October 2007 to less than $7. Its dividend would be reduced from $1.24 to $0.82, and its once sterling AAA credit rating would fall seven levels to the BBB tier.[9],[10]

External Factors: Industry and Consumer Trends

In the early 2000s, GE started to face new issues with vendors, suppliers, and consumers. As a consequence of globalization, wages around the world were rising. To remain competitive, GE outsourced its manufacturing to South Korea to reduce costs. This technology transfer provided Asian companies with an opportunity to introduce lower-cost comparable products, and this left GE scrambling because they never imagined their loyal customers would leave their brand. Looking for the next big thing, GE decided to create an elevated line of products to reach more sophisticated consumers with different customer experiences. GE’s dependencies on other suppliers for raw material had a significant impact on their bottom line. The weak performance of GE Oil and Gas could be attributed to raw material fluctuation in the Asian markets. To avoid such fluctuations, GE had to develop a rigorous supply change management program that would align with the organization’s financial goals.

Around the same time, unicorn companies[11] began to emerge in the tech ecosystem. There was an increasing trend among large enterprises to acquire these highly-valued startups as a means to access their bleeding-edge technology or acquire their top talent. The adoption of data analytics, machine learning, and artificial intelligence to improve operational capabilities was on the rise. This was demonstrated by the heightened demand and utilization of IoT devices in the manufacturing industry. IoT devices allowed firms to capture and process operational data in real-time, leading to increases in overall efficiency and effectiveness. To be on par with the emergent tech giants, Jeffrey Immelt was in constant dialogue with CEOs like Jeff Bezos, Marc Benioff, Steve Ballmer, and Satya Nadella to gain insights into emerging technology trends and innovations. As GE was trying to adapt to the latest high-technology trends, consumers were transitioning to more renewable energy sources compared to coal and oil-based sources for their everyday energy needs. As described by the Annual Energy Outlook of 2012, “State RPS programs [and] State RPS policies are not the only driver of growth in renewable generation.”[12] Consumers were willing to spend more on appliances if it saved energy costs on the whole. Aligning with these industry trends, GE’s competitors, including Siemens, Hitachi, 3M, and United Technologies,[13] established innovation programs around sustainable energy solutions.

Change Drivers

In 2012, GE faced several fundamental business challenges: (1) the emergence of a new paradigm in the business landscape, (2) the commoditization of its legacy business lines, and (3) the long lead-times and high-cost of innovation inherent in its capabilities. These were the principal drivers behind the GE FastWorks transformation.

A Changing World: A New Paradigm of Speed and Customer Centricity

The new century marked what many observers considered a turning point in business. After taking the CEO role, Immelt slowly began to experience a paradigm shift away from a world where GE enjoyed pillars of competitive advantage—a world of scale—towards a world where GE was ill-suited to compete—a world of speed.

In this new world, symbolized by the Silicon Valley Entrepreneur, businesses leveraged technology combined with iterative, customer-centric development processes to outpace and out-innovate their more established competitors like GE. Around this time, Clayton Christensen coined the theory of disruptive innovation. He warned that large, established companies like GE optimize too heavily for existing customers and dominant product patterns. Consequently, these companies ignored adjacent unexplored customers and product patterns, leaving space for startup challengers to introduce products that are orders of magnitude simpler, better, or cheaper. The eventual result was that these existing businesses would face growing competition that would eventually overwhelm them.[14] Immelt was moved by the widely read WSJ article, Why Software Is Eating the World, in which its author, Marc Andreessen, predicted: “We are in the middle of a dramatic and broad technological and economic shift in which software companies are poised to take over large swathes of the economy.”[15] Immelt saw GE's opportunity to capitalize on its existing advantages while making a turn towards the new paradigm. “My view was that GE had as good a chance as anybody at winning in the industrial internet because we were not starting from scratch: We had a $240 billion installed base of service contracts, a huge order backlog, and the ability to offer financing. We could build on our existing strengths to get even better. So we launched digital across all our businesses. By that, I mean we launched a major effort to embed sensors in our products and build an analytics capability to help our customers learn from the data that the sensors generated.”[16]

Commoditization of Legacy Businesses

An assessment of GE shows a position heavy in business lines that could mostly be categorized as commodities. Commodity businesses are generally high-volume, operationally-focused organizations. These sorts of enterprises face both decreasing margins and the threat of disruption.

GE’s Capabilities

In line with the new paradigm, an assessment of GE’s capabilities showed particular challenges experienced in GE’s high-profile innovation programs: long lead-times, high-cost, and lackluster results.[17]

Our customers and our employees were both telling us, ‘Love the company, but it’s slow.’ Our customers were saying, ‘You guys are a little bit too hard to do business with.’ Our employees were saying, ‘We want to do a better job working with our customers.’ It was coming from a number of different places, but all recognizing that the world was fundamentally changing, and if we were to continue to be in existence, we had to change our culture and our solutions for our customers, how we work with our customers, how we think, and how we operate.

--Janice Semper, a leader of GE’s cultural transformation [18]

FastWorks and Culture Change Process

In 2012, Immelt had a strategic vision to reset, reboot, and reinvigorate GE’s failing engine. There was a desire to migrate away from their traditional way of operating and to inject a significant amount of startup DNA into their way of working. His proposed changes would value customer-centricity and leanness. Immelt wanted to promote a faster pace of innovation as a means to address the present and future needs of consumers and the wider market as a whole.

Eric Ries and The Lean Startup

While Immelt was ruminating on how his organization could change its stripes, GE team members Viv Goldstein and Beth Cornstock met Eric Ries during the release of his book, The Lean Startup. The book highlighted Ries’ product development methodology, which utilized contemporary techniques favored by Silicon Valley startups that emphasized three key themes: efficiency, effectiveness, and customer-centricity. The lean startup methodology prioritized (1) experimentation through the testing of hypotheses, (2) iterative processes, (3) continuous feedback, (4) validated learning, and (5) pivoting to address concerns. It attempted to provide a generally applicable product development model grounded in entrepreneurship to all sectors of business. Goldstein and Cornstock felt that this methodology and its author, Ries, addressed Immelt’s desire to apply the principles of entrepreneurship and innovation more systematically at GE.

Ries came to GE and started asking questions regarding whether a product should be built as opposed to if it was possible to build a product. This line of questioning forced GE to focus on customer needs and opened a dialogue around how they could make their product development process more efficient and effective. After a series of workshops, GE leadership realized that a more transformative culture shift was necessary to implement lean startup principles and practices at GE properly. These workshops would ultimately give way to the creation of FastWorks—a process for how GE would design products through experimental design, faster product release cycles, and leveraging customer feedback to continuously improve its products.

Culture Change Methodology

The figure below describes the framework of FastWorks. It encourages “providing tools for growth” and “applying the mindset every day.”[19]

GE’s culture shift in the form of this process was an attempt to “shorten product development cycles by eliminating waste and focusing on quality and cost control.”[20] GE wanted to own the process and build internal buy-in, so the organization created its own program, adopting lean startup principles into its business processes. The process was designed to ensure alignment across all business units, but each unit was to have enough flexibility and freedom to adapt its practices to their specific needs.

After FastWorks was co-founded by GE’s Goldstein (Business Innovation) and Janice Semper (HR), they, along with Ries and David Kidder (author of The Startup Playbook), embarked on a roadshow to train senior leadership. Over 5,000 GE leaders were trained during this time in 2-day workshops.[21] The transition from Welch’s Six Sigma to FastWorks was anticipated and proved to be a challenging situation for many GE employees. The process focused on four key concepts: “discover, develop, learn and act” and highlighted creativity, failure, and non-linear processes which was a significant shift from the linear focus of Six Sigma.[22] The FastWorks team started training external coaches who were tasked with building capacity internally in GE as a pivot to the challenging learning situation for employees.[23]

In January 2013, GE launched the first FastWorks project around a refrigerator with a newly created cross-functional team. Initially, customers did not like the product, and it took five iterations before customers started responding positively. That being said, it was reported that the team developed a refrigerator in half the time and financial resources it normally cost GE to develop a refrigerator. The pilot greenlit the spread of the FastWorks program for the entire organization. In a few years, there were hundreds of FastWorks programs throughout the organization.[24]

Challenges During the Culture Shift

As GE underwent this culture shift, the organization faced internal and external challenges alike, including activist investors, bad strategic investments, and the role that innovation would play in GE's traditional business units.

Activist Investors

The main challenge was the presence of an activist investor. In 2015, Nelson Peltz’s Trian Fund Management LP bought a 1.5% stake in GE (valued at $2.5 billion) and followed up with public criticism of the company in the form of a white paper titled Transformation Underway...But Nobody Cares.[25] The paper outlined Peltz’s belief that the company’s current culture shift and other such transformations were not beneficial for GE and its shareholders. Lack of investor confidence was demonstrated by its undervalued stock price. Peltz argued that GE’s senior leadership team was not placing shareholder value above its other priorities. Trian Partners advocated for a series of actions that would increase shareholder value and return dividends to investors:

- Take on $20 billion in debt to buy back stock as a means to return cash to shareholders

- Purchase more than what was already committed to in its existing repurchase plan ($50 billion)

- Cut expenses to increase operating margins by up to 18%

Immelt believed that the actions suggested by Trian Partners would have had short-term, positive impact on shareholder value, but a negative impact on GE’s long-term health and its investment in innovation. Therefore, he held off on following the actions suggested by Peltz and Trian. Unfortunately, “GE’s board was not happy with the company’s margins and stock price, or how Wall Street viewed its future. The immediate threat of a proxy fight with an activist investor forced a decision on the future direction of the company.”[26]

Bad Strategic Investments

During the culture shift, GE made a strategic decision to double down in the electrical power sector with its acquisition of Alstom. GE was interested in the French electrical generator company’s transportation business in the form of gas-powered turbines. Internally and externally, the purchase was seen as a strong move that would expand the horizontal reach of GE Power across the world and potentially meet an increase in the commercial need of generators across different contractors for GE’s business units. Unfortunately, demand for gas-powered turbines was not as strong as predicted due to increased interest in renewable energy sources. As a result, GE was forced to cut costs to adjust for its bad investment. A lousy bet in a single sector led to ramifications throughout the organization. After all, despite its push to innovate, improve, and grow, GE was “getting better and better at things customers wanted less and less. That's how you get disrupted.”[27]

Section 2: Analysis and Recommendation

Diagnosis of GE from 2012 to 2016

Mission, Vision, and Strategy

In 2012, GE had a broad, overly-diverse portfolio which lacked asset efficiency. Its non-industrial businesses were low-tech, slow to innovate, and its business units operated in silos. Although GE's strategy was to be an efficient and lean company and an industrial conglomerate leader, its market share, sales, and profits were declining year over year. This triggered the need for change, which led Immelt to adopt the lean startup-inspired program, FastWorks, and divest slow, inefficient, and non-industrial businesses. To align its vision and mission, GE developed a strategy that was focused on customer and continuous innovation. They wanted to think long-term by investing in people with a focus on training and professional development. By 2016, the adoption of lean startup methodologies changed GE’s product development strategy from "Can the product be built?" to "Should the product be built?", helping GE avoid distractions and waste.[28]

Structure

As explained above, in 2012, business units worked in silos with no alignment between their functions. GE’s structure was centralized, and its regional businesses had no autonomy in their decision-making process. This resulted in slowness and inefficiency. To align the business and overcome its complex vertical structure, GE established the Global Growth Organization (GGO). GGO expanded GE’s presence in emerging markets and created horizontal operations with shared P&L responsibilities. This enabled stream alignment between business units with a shared vision, allowing GE to be more aligned and achieve their common goals by 2016.

Decisions

In 2012, decisions were made by a centralized corporate executive team—especially when it came to resource allocation and alignment with financial planning cycles and market opportunities. This could have helped shape their corporate agenda and control funds, but it instead created bottlenecks in decision-making. Additionally, the lack of a feedback loop from customers and the wider addressable market led to the prioritization of “the wrong” projects. This changed drastically by 2016 wherein decentralized decision-making placed a greater emphasis on local market needs. By introducing products to the market earlier, valuable customer and market insights could be obtained ahead of industrialized mass production. The incorporation of customer feedback and recommendations into the product development cycle helped increase efficiency and lower costs.

Process and Policies

In 2012, the process and policies at GE encouraged a waterfall methodology. Large programs of work were designed up-front and project responsibilities were handed-off from one functional area to the next. Quality was enforced by reducing variability, economies of scale, statistical control, and annual performance evaluation. By 2016, GE’s processes and policies promoted an agile methodology that inculcated a highly iterative and scientific approach to product development. There was an emphasis on having a portfolio of innovation projects that leveraged rapid experimentation.

Technology

While most of the innovation from the early 2000s was focused on consumer and communications technologies (e.g., the development of smartphones, tablets, social media platforms, etc.), in 2012, GE felt the need to develop and install sensors within all of their devices as their technology became outdated. This would provide GE products with real-time data collection and analysis capabilities, allowing for data-based optimizations. GE was one of the early adopters of IoT technology into its machinery and, by 2016, most of its new products included IoT sensors. This culminated in the launch of GE’s Predix Platform—a data analytics tool that could bring immense value to customers.

Performance Metrics

Personal Prior to 2012, employees at GE were rewarded for risk aversion and on delivery of promised outputs. The organization was more managerial and employees had very little to contribute in decision making. By 2016, performance metrics of employees were more customer and product-focused which helped promote a culture of innovation.

System In 2012, the Human Resources evaluation was mostly based on ROI, cost reduction, increase in market share, margins, incremental growth, and entitlement funding. This changed drastically by 2016 as GE re-engineered performance appraisals to encourage innovation that was more customer-focused.

Capabilities (Agility)

In 2012, GE lacked the agility to build capabilities for innovation unlike modern technology companies like Amazon and Facebook. Prior to FastWorks, it took two to three years before design flaws were discovered or customer adoption of a product was known. Conversely, modern technology companies focused on putting Minimum Viable Products (MVP) into the market to gauge customer reactions with minimal investment. By 2016, GE developed faster go-to-market capabilities and started to collect customer feedback, which gave them time to incorporate changes suggested by customers before product launch.

Leadership/Talent

The leadership at GE prior to 2012 was top-down, where all decisions were made at the higher-levels, and execution was carried out at lower-levels with little to no employee involvement. The talented engineers were required to only engage in predictive engineering and could not work on other riskier projects. To implement FastWorks, the company needed new talent, and Eric Reis seemed to be that person who, as an external consultant, could introduce Lean Startup methodologies to GE. By 2016, these changes encouraged GE to have a top-down/bottom-up leadership. Additionally, they adopted Silicon Valley trends like two-pizza teams and employing a founder’s mentality.

Culture

Prior to 2012, GE’s culture was archaic. Innovation was very predictive with little to no encouragement towards customer-focused product evolution. The organization had become too compliance-focused which in turn hindered innovation. By 2016, after FastWorks, GE was able to adopt a culture of failing fast and early which promoted innovation and encouraged development teams to collaborate more effectively with customers.

Goal Alignment

In 2012, with the introduction of FastWorks, Immelt was able to garner the support of his business units and embark on a transformative change program. GE took a leap towards innovation accounting, leading indicators, and meetered funding. Despite this, by 2016, a deep drop in stock price raised eyebrows in some business units. GE started to consider a change in leadership and the decommissioning of the FastWorks program.

Analysis

If one looks back at the history of GE, it seems so surprising that a company that was once the darling of big conglomerates is now no longer part of the Dow Jones Industrial Average. So what went wrong? Based on our analysis, we believe that GE’s strategic shift toward FastWorks in 2012 was not a bad idea but, we do feel it should not have been applied broadly all over GE, and actually set back the company even further. When analyzing the change through the lens of the organizational model, one would think that a lot of things were done right, but the issue wasn’t necessarily how GE went about adopting FastWorks, it was whether they should have done so in the first place.

In 2012, GE was in a crisis situation with declining year-over-year revenues and lackluster profit margins. In order to drive confidence among the investor community, GE needed to drive shareholder value and profitability. Instead, Immelt implemented a program that would take years to reap any significant benefits. The Lean Startup Method was intended for companies that were in good shape and looking to drive future innovation to continue its success. GE was an old company with many commoditized products with little room for growth through innovation. Thus, the timing of FastWorks implementation missed the mark completely.

Immelt attempted to adopt FastWorks like Jack Welch adopted Six Sigma by investing significant time, energy, resources, and training behind it. They trained thousands of leaders and expected broad adoption throughout the organization. He attempted to drive a 180 degree turn away from a slow, methodical approach to innovation with a focus on efficiency and low risk, to an iterative, high risk approach that wasn’t comfortable for a 125 year old hierarchical organization. He also attempted to “boil the ocean” by implementing it broadly across all businesses; even those that were older and less reactive to innovation. Thus the ability to drive additional shareholder value was limited through FastWorks implementation.

Recommendations

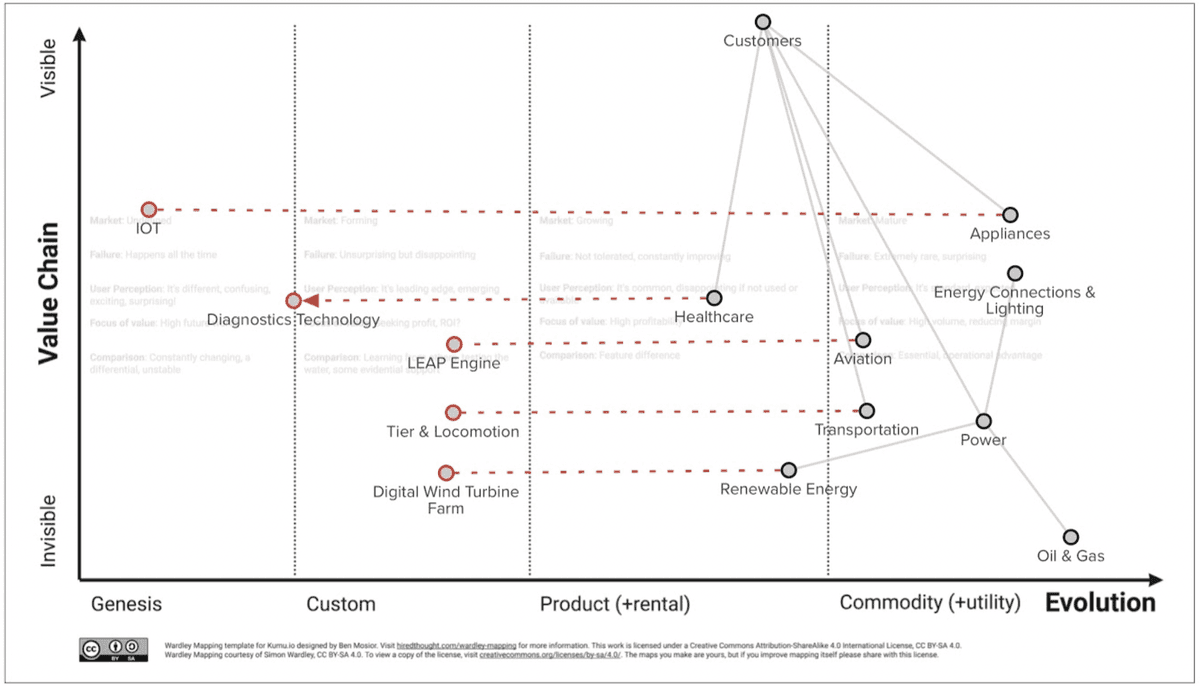

In order to turn the situation around at GE, we have a few recommendations. First, instead of abandoning FastWorks, GE should apply it to the businesses that would benefit from a more iterative innovation process. We recommend that GE invest in newer businesses such as renewable energy and IoT, as these are two areas that make sense for GE to continue their FastWorks efforts. Focusing their attention in both of these areas would provide GE with (1) a higher potential return on its innovation investments and (2) an opportunity to move further up the value chain (see appendix exhibit “Recommendation Wardley Map”).

Next, it will be important for GE to better manage key internal and external stakeholders. Internally, they should focus their FastWorks training and execution efforts on those who are most valuable to the MVP development process, provide them with the runway to create, and get out of their way to drive faster-paced innovation. For the business verticals that would not benefit from FastWorks execution efforts, GE should work to significantly reduce costs to drive profitability. Externally, we recommend GE management should engage and communicate with external stakeholders to have a joint working strategy so that their recommendations are incorporated.

Finally, we recommend that GE commit to innovation as a strategy and avoid making additional “big bets” in the commodity spaces within which they operate. For example, no more acquisitions of companies like Alstrom. They should focus their attention on driving innovation in the business lines that can drive bottom line profitability and growth for GE.

Appendices

Recommendation Wardley Map

Timeline[29]

▩ GE Market Capitalization ▩ Dow Jones Industrial Average

-

1981

- Jack Welch becomes the youngest chairman and CEO in GE’s history. Welch’s strategy for turning around General Electric was performance management and operational efficiency, favoring speed to market, simplicity, and self-confidence.

-

1982

- Welch disassembles the leadership team and structure left behind by his predecessor Reginald H. Jones. Welch’s intention is to dismantle bureaucracy and improve communication. He believes involving employees in the quality process greatly benefits the organization.

-

1995

- Welch adopts Motorola’s Six Sigma methodology, placing a large focus on quality and operating efficiency.

-

1998

- GE’s revenues reach $100 billion for the first time. This is largely the result of GE’s transition away from its manufacturing roots. Welch transformed GE into a $100 billion conglomerate with holdings spread across various sectors and industries, including but not limited to aerospace, appliances, credit and mortgage services, insurance companies, media, plastics, power, information technology, and transportation.

-

2001

- Jeffrey Immelt takes the helm as CEO of GE just as the dot-com bubble bursts and terrorists attack the US on September 11th.

-

2003

- Steve Blank publishes Four Steps to Epiphany which forwards the idea that startups are not just smaller versions of big corporations. He begins teaching a customer-driven development methodology at the Haas School at University of California, Berkeley.[30]

-

2004

- Blank invests in Eric Ries and Will Harvey’s startup, IMVU. Ries and Harvey attend Blank’s course as a condition of the investment. Ries coins the term lean startup. It is a discipline that combines lean manufacturing, iterative agile techniques, and a focus on customer-driven development.

-

2008

-

Amid the worst recession since the Great Depression, GE receives $139 billion in government loan guarantees to shore up its capital arm and raises $15 billion through an emergency stock sale, a fifth of which comes from billionaire Warren Buffett. The company may not survive the financial

-

GE’s outstanding debt reaches its peak at more than $500 billion.

-

-

2009

- GE’s stock price falls to less than $7 (from $42 in October 2007) and its dividend is reduced to $0.82 (from $1.24). The company loses its sterling AAA credit rating, falling seven levels into the BBB tier.

-

2010

-

Prescott Logan, GM of GE’s Energy Storage Division begins applying lean techniques for his industrial battery product line. Logan searched for a business model and engaged in active customer discovery. They used myriad customer feedback to narrow their focus and targeting, eventually settling on cell phone providers in developing countries with unreliable electric grids.[32]

-

Literature around startups and lean methodologies emerge. Osterwalder and Pignauer publish Business Model Generation.

-

-

2011

- Ries publishes The Lean Startup.

-

2012

- Blank and Dorf publish The Startup Owner’s Manual. GE senior management teams up with Eric Ries to create the FastWorks program. Ries trained 80 Lean Startup coaches exclusively dedicated to GE’s FastWorks program. Together they exposed almost 1,000 GE executives to Lean Startup principles.[33]

-

2015

-

GE acquires Alstom, a large French competitor to GE Power. GE funnels large amounts of money, time, and development on gas turbines. As a result of regulatory changes made during acquisition close, the addition of 30,000 high-cost employees, and the emergence of competing renewables, GE Power’s profit plunged 45%.

-

Trian Partners, an activist investor, buys $2.5 billion of GE stock (approx. 1.5% of the company). Trian argues that GE should optimize for increasing stock price (i.e., via cutting expenses, buying back more stock) which could endanger GE’s long-term investment in innovation.[34]

-

-

2016

- GE’s home appliance division, one of its best-known brands, is offloaded to China’s Haier Group for $5.6 billion. Since 2010, the company has sold off more than $140 billion worth of businesses. Instead of using the proceeds to pay off its debt, it funds massive share buybacks.

-

2017

- Jeffrey Immelt resigned as CEO of GE. Trian Partners receives a seat on the GE board.

-

2018

- GE removed from the Dow Jones Industrial Average after a 100 year legacy.

Bibliography

[1] A full timeline of GE and its FastWorks transformation can be found in the Appendices.

[2] https://www.nytimes.com/1985/05/05/business/why-jack-welch-is-changing-ge.html

[3] https://en.wikipedia.org/wiki/Six_Sigma

[4] http://www.annualreports.co.uk/HostedData/AnnualReportArchive/g/NYSE_GE_1998.pdf

[5] https://review.chicagobooth.edu/strategy/2019/article/three-strategy-lessons-ge-s-decline

[6] https://www.cnbc.com/2008/11/12/ge-capital-approved-for-fdic-liquidity-program.html

[7] https://archive.fortune.com/2008/10/09/news/companies/colvin_ge.fortune/index.htm

[8] https://www.nytimes.com/2008/09/22/business/22ge.html

[9] https://abcnews.go.com/Business/story?id=7076145&page=1

[10] https://www.wsj.com/articles/what-ge-needs-to-do-to-avoid-junk-territory-11547042400

[11] A privately held startup company valued at over USD 1 billion.

[12] https://www.eia.gov/outlooks/aeo/pdf/0383(2012).pdf

[13] https://www.forbes.com/sites/narrativescience/2012/01/17/forbes-earnings-preview-general-electric

[14] https://hbr.org/2015/12/what-is-disruptive-innovation

[15] https://www.wsj.com/articles/SB10001424053111903480904576512250915629460

[16] Jeffrey R. IMMELT in HBR, Sept. 2017, https://hbr.org/2017/09/inside-ges-transformation

[17] Ries, E. (2017). The startup way: how modern companies use entrepreneurial management to transform culture and drive long-term growth. First edition.

[18] Semper, Janice. “Collaboration Speeds Up at General Electric” MIT Sloan Management Review, https://sloanreview.mit.edu/article/collaboration-speeds-up-at-general-electric

[19] http://www.edgef.org/wp-content/uploads/2016/08/GE-Innovation-and-FastWorks-Presentation-v6.pdf

[20] https://www.barnesdennig.com/ge-aviations-fastworks-program-shows-how-big-companies-can-act-small/

[21] https://www.collectivecampus.io/blog/how-ge-saved-80-in-development-costs

[22] https://leanstartup.co/fastworks-reflecting-origin-evolution/

[23] https://academy.nobl.io/how-ge-implemented-fastworks-to-act-more-like-a-startup/

[24] https://hbr.org/2014/04/how-ge-applies-lean-startup-practices

[25] https://www.wsj.com/articles/BL-263B-6136

[26] https://hbr.org/2017/10/why-ges-jeff-immelt-lost-his-job-disruption-and-activist-investors

[27] https://www.inc.com/greg-satell/how-ge-got-disrupted.html

[28] This diagnostic leverages the Shared Vision and Goal Alignment Organization Model.

[29] Image taken from https://www.bloomberg.com/graphics/2019-general-electric-rise-and-downfall/.

[30] https://hbr.org/2013/05/why-the-lean-start-up-changes-everything

[31] https://www.cnbc.com/2008/11/12/ge-capital-approved-for-fdic-liquidity-program.html

[32] https://hbr.org/2013/05/why-the-lean-start-up-changes-everything

[33] https://www.ge.com/news/reports/the-biggest-startup-eric-ries-and-ge-team-up-to

[34] https://steveblank.com/2017/11/01/why-ges-jeff-immelt-lost-his-job-disruption-and-activist-investors/